You probably know what your pension will look like, roughly speaking. Maybe you’ve checked your projected Social Security amount, glanced at a statement, or listened to a coworker complain about their retirement income. It all feels straightforward. The numbers are set. Nothing will change.

Here’s the thing though. What if you’ve been underestimating what retirement looks like where you live? There are aspects of state retirement benefits that don’t show up on your typical online calculator or annual summary. Some of these hidden layers add thousands to your net income every single year. Others quietly preserve the buying power of your pension long after you retire. Let’s dive in.

Investment Returns Bounced Back Sharply in 2023

After a rough 2022, state pension plans saw investment performance improve dramatically. According to data from Wilshire TUCS, the median plan saw a significant increase from a -7.77% return in 2022 to 8.32% in 2023, as reported by The Pew Charitable Trusts. This rebound helped stabilize funding levels after a difficult year.

What does that mean for you? Stronger investment returns reduce the risk that your state has to cut benefits down the road or reduce cost-of-living adjustments. For millions of retirees, that kind of stability is reassuring even if they never hear about the behind-the-scenes recovery.

Public Pensions Still Struggle Below the Resilience Threshold

Even with 2023’s strong showing, state retirement systems remain under stress. Between 2023 and 2024, the average market valued public pension funded ratio increased from 75.5% up to 80.2%. This marks 17 consecutive years with an average funded ratio below 90%, the minimum threshold for pension plans to be considered resilient, according to Equable’s State of Pensions 2024 update.

Think about that for a second. For nearly two decades, the systems designed to protect public workers’ retirements have been weaker than financial experts recommend. Most people assume pensions are bulletproof. They aren’t always. The long-term strain shows how fragile some state promises can be if investment returns disappoint or contributions fall short.

Your Pension Loses Value Faster Than You Think Without COLAs

Here’s a number that sticks. As of June 30, 2023, there is a national public pension funding shortfall of around $1.49 trillion, according to Equable Institute data. Let’s be real though. That trillion-dollar gap is hard to visualize. What matters more is what inflation does to your actual purchasing power every single year.

NASRA provided an eye-opening illustration in their 2025 COLA issue brief. If a retiree starts with a twenty-five thousand dollar annual pension and inflation runs at a steady three percent with no cost-of-living adjustments, that same benefit shrinks to about eighteen thousand five hundred dollars in today’s money after twenty years. Cost-of-living adjustments in some form are provided on most state and local government pensions, which is why these quiet annual bumps can feel generous over time even if you didn’t notice them at first.

Most State Plans Quietly Offer Some Form of COLA Protection

If you’re enrolled in a state or local pension plan, chances are your retirement check won’t stay frozen in place forever. Approximately three-fourths of pension plans sponsored by states and local governments provide some form of an automatic cost-of-living-adjustment, according to NASRA.

These adjustments happen differently depending on where you work. Some plans tie increases directly to the consumer price index. Others set a fixed cap, say two percent a year. Still others make the annual bump conditional, based on how well the pension fund’s investments performed. You might not realize it, but that flexibility means your retirement is far more dynamic than a single benefit number suggests.

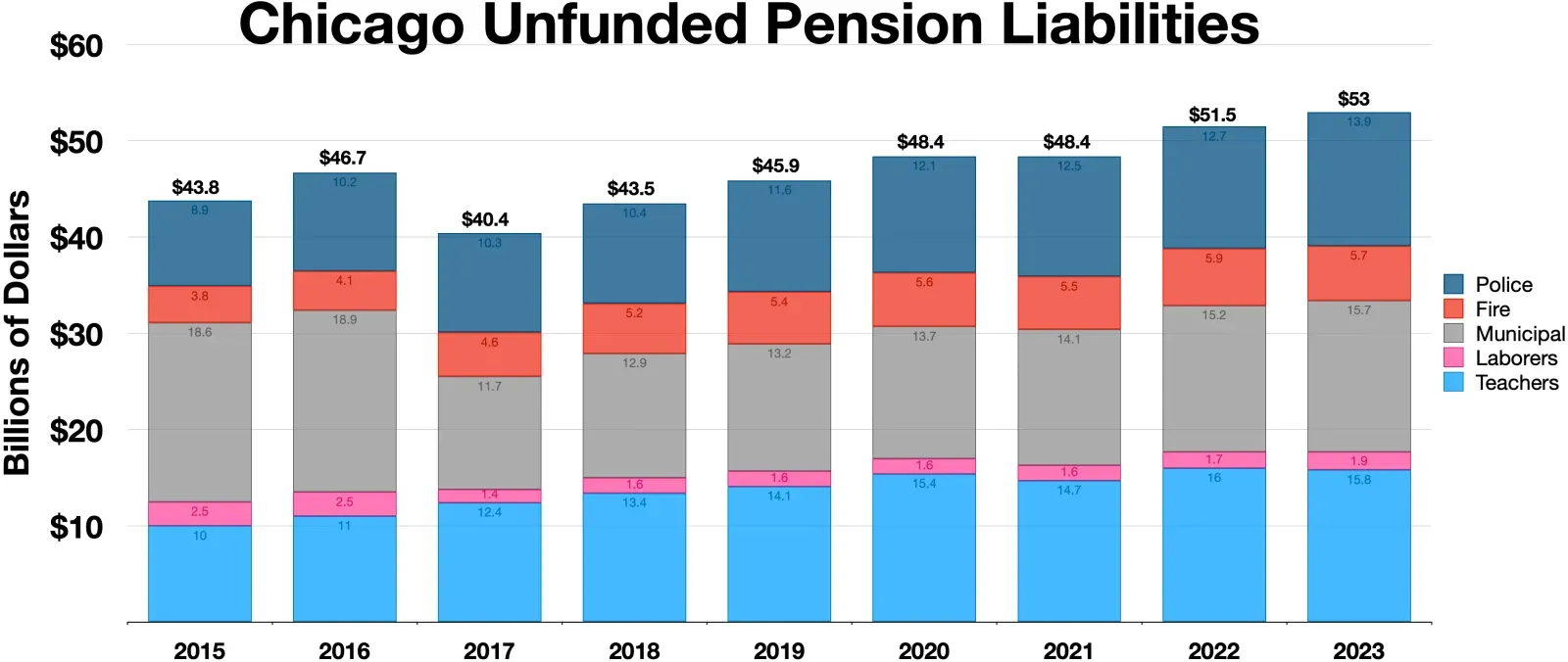

Unfunded Pension Liabilities Are Massive Even Under Reported Figures

Here’s something worth knowing, even if it doesn’t show up in your annual benefit statement. Unfunded pension liabilities across state and local systems remain staggering. For fiscal year 2023, there is a national public pension funding shortfall of around $1.49 trillion. Collectively that is just 77.4% of the money that should be in state and local pension funds today, according to Equable’s analysis.

That shortfall doesn’t mean your check is in danger tomorrow. Still, it highlights how much future taxpayer dollars may be needed to cover promises already made. Some policy researchers use even higher estimates when they calculate liabilities using market-based methods instead of the assumptions pension funds report. Either way, the sheer size of the gap puts pressure on state budgets and shapes decisions about future benefit structures.

The U.S. Hit a Record Retirement Wave in 2024

Timing matters when it comes to retirement benefits. The Social Security Fairness Act, which was signed into law on January 5, 2025, repealed the WEP and GPO, according to Minnesota’s Legislative Commission on Pensions and Retirement. This repeal changed the game for public employees who previously lost Social Security benefits because they received a government pension. Suddenly, thousands of retirees saw benefit increases they hadn’t expected.

Meanwhile, roughly four million Americans turned sixty-five in 2024, a pace expected to continue through at least 2027. This surge means pension systems are under more pressure than ever to deliver. The silver lining is that state systems have been aware of this demographic shift for years and many adjusted their funding strategies accordingly.

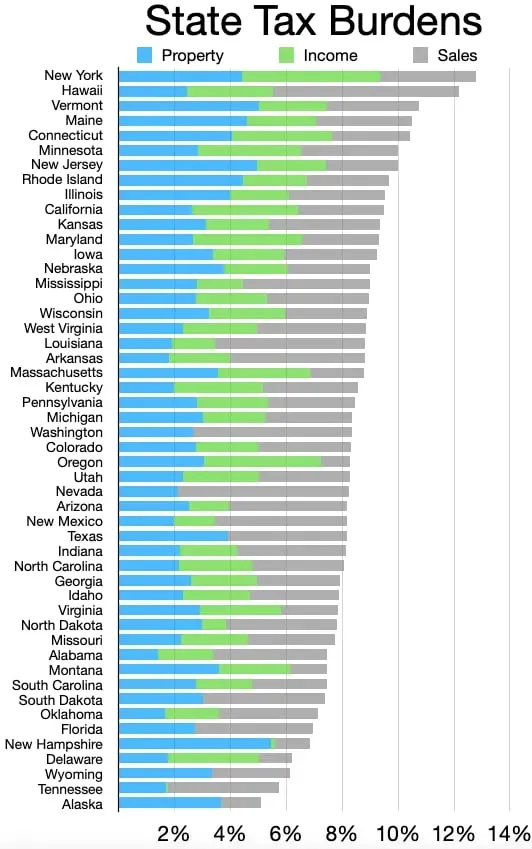

State Tax Treatment Can Make Your Retirement Income Feel Far More Generous

Let’s talk about something that rarely gets enough attention. The state where you retire can matter more than the size of your pension check. State taxation of retirement income differs significantly across the U.S. Some states completely exclude retirement earnings from taxes, while others apply varying levels of taxation to pension payments, IRA and 401(k) withdrawals, military retirement pay, and Social Security benefits, according to Empower’s 2025 summary.

Imagine two retirees with identical pension amounts. One lives in a state that taxes all retirement income. The other lives somewhere that exempts pensions entirely. The second retiree takes home thousands more every year without any change to the actual benefit. That’s not theoretical. It happens every single day across the country.

Some States Explicitly Exempt Major Forms of Retirement Income

You might be surprised how many states don’t tax your pension or retirement account withdrawals at all. In addition to the nine states above that don’t have an income tax at all, four states do not tax retirement income: Illinois, Iowa, Mississippi and Pennsylvania, according to Bankrate.

That exemption applies to distributions from traditional pensions, 401(k) plans, and IRAs, as long as you follow the plan’s requirements. Nine states levy no general state income tax at all, meaning they won’t tax your retirement income or pension: Alaska, Florida, Nevada, New Hampshire (effective 2025), South Dakota, Tennessee, Texas, Washington, and Wyoming, according to Taxfyle. If you planned your entire career in one of these places, you’re benefiting from a level of tax relief that many retirees elsewhere can only dream about.

Average Social Security Benefits Vary Significantly by State

Social Security is supposed to be a federal program with uniform rules. Yet the checks retirees receive vary widely depending on where they worked and lived. In November 2025, the average monthly Social Security check for retired workers was $2013.32, according to Kiplinger.

Connecticut ($2,196.15), New Jersey ($2,190.05), New Hampshire ($2,183.82), Delaware ($2,170.63) and Maryland ($2,139.54) have the five highest average Social Security monthly checks. Mississippi ($1,814.24), Louisiana ($1,818.40), Arkansas ($1,852.07), New Mexico ($1,865.12) and Kentucky ($1,865.76) have the five lowest average monthly benefits. That’s a difference of nearly four hundred dollars a month between the top and bottom states. Over a twenty-year retirement, that adds up to roughly ninety thousand dollars more for someone in Connecticut compared to someone in Mississippi.

State Tax Rules Can Change Recently and Materially

Sometimes generosity comes from new legislation you didn’t even know was being debated. Iowa recently made retirement income tax-exempt for residents 55 and older and eliminated its inheritance tax for tax years 2025 and later. For 2025, Iowa moved to a flat tax rate of 3.8%, according to Kiplinger’s state tax guide.

Louisiana made similar moves. The state shifted to a flat three percent income tax effective January first, 2025, along with additional retirement income exclusions for seniors. These kinds of changes don’t just tweak the margins. They can shift a retiree’s annual take-home income by thousands of dollars almost overnight, changing what “generous” actually means in practice.

What do you think about how much retirement benefits vary by state? Did you expect such big differences? Tell us in the comments.