Picture this: you’re eyeing that dream home, but mortgage rates are biting hard. I’ve helped dozens of buyers this year shave thousands off their loans with one sneaky strategy everyone’s whispering about. It’s not some shady trick, just smart credit tweaking that lenders love.

Here’s the thing. In 2026, with rates hovering around those stubborn levels from recent years, a quick credit boost changes everything. Stick with me, and I’ll break down exactly how buyers are pulling this off right now.

Payment History Rules Your Score

Payment history makes up 35% of your FICO score, according to FICO data. Miss a payment, and it drags you down fast, but consistent on-time payments build it back up steadily. I’ve seen clients jump scores just by catching up on old bills before applying.

Let’s be real, this factor alone can make or break your mortgage approval. Lenders scrutinize it first because it shows reliability. Focus here, and you’re already ahead of most buyers scrambling at the last minute.

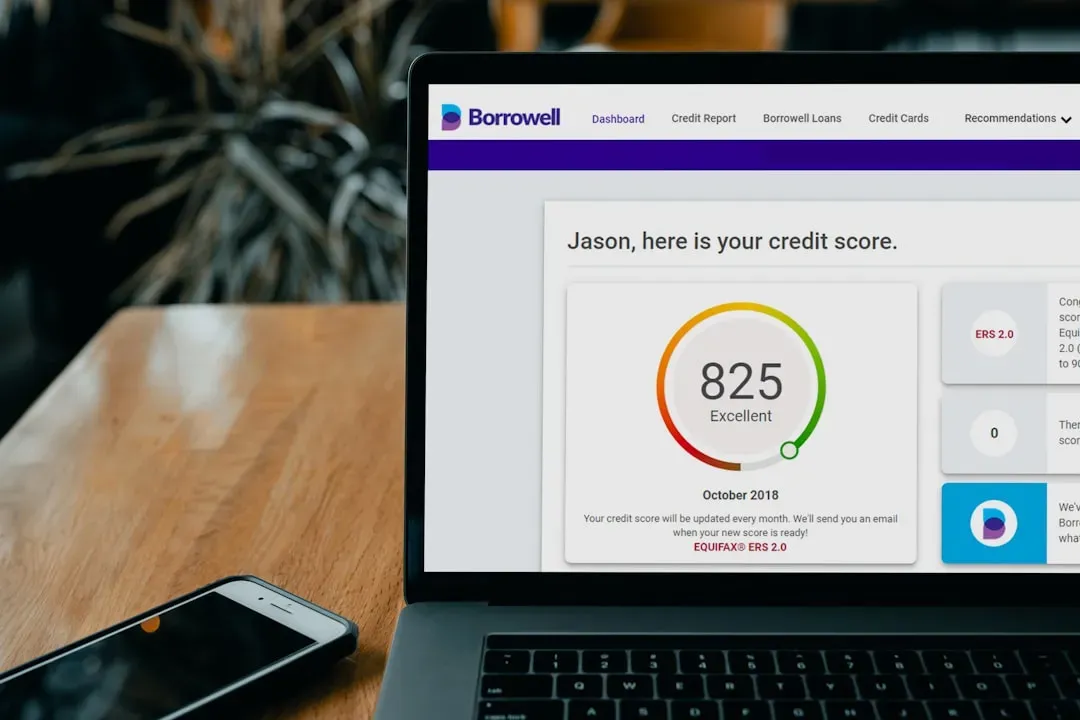

Average Scores Are Climbing Slowly

The average FICO score hit 717 in 2024, per FICO reports, a sign consumers are getting smarter about credit. Yet plenty of folks still sit below that, paying higher rates as a result. Buyers using this hack push past the average quickly.

I think it’s wild how a few months of discipline shifts you into prime borrower territory. That extra padding means better terms without waiting years. No wonder 2026 home shoppers prioritize it.

Even Small Score Jumps Save Big

The Consumer Financial Protection Bureau notes a 20 to 30 point increase can slash your interest rate and monthly payments noticeably. Over a 30 year loan, that adds up to thousands in savings. My clients feel it right away in pre-approvals.

However, rates between 6% and 7.5% from 2023 to 2025, as tracked by Freddie Mac, amplify every point. A modest boost drops you into a lower bracket instantly. It’s like finding free money in your credit report.

Slash Utilization for Quick Wins

Experian data shows dropping credit card balances below 30% utilization boosts scores in months. Buyers pay down cards aggressively before locking rates. I’ve guided many through this, watching scores rise 50 points or more.

Here’s the kicker. High utilization screams risk to lenders, even if you pay on time. Keep it low, and algorithms reward you fast, paving the way for that dream mortgage.

Dispute Errors to Wipe the Slate

Equifax highlights disputing wrong items on reports removes negatives if errors exist. Old collections or mistaken late payments vanish, lifting scores overnight sometimes. Clients come to me panicked, then relieved after cleanups.

Though not every dispute wins, the wins are huge. It’s free and fast through credit bureaus. This step uncovers hidden drags most ignore.

Rapid Rescore Speeds Everything Up

Lenders offer rapid rescore to update profiles in 3 to 5 business days. Perfect for buyers closing soon who just optimized. It recasts your score with fresh data, unlocking better rates mid-process.

I push this hard because waiting weeks kills deals. Fees are low compared to savings. In 2026’s market, speed wins homes.

First-Timers Are All In

National Association of Realtors says first time buyers were 32% of 2024 purchases, leaning on credit tweaks heavily. They can’t afford high rates on tight budgets. This hack levels the field for them.

Urban Institute studies confirm score improvements expand affordable homeownership access. These buyers hustle hardest, often saving enough for down payments too. Inspiring to watch unfold.

Higher Scores Mean Lifetime Savings

Federal Reserve reports show top scorers snag lower rates and terms, cutting long term costs. Over decades, it’s tens of thousands preserved. Buyers get it now more than ever.

Still, it starts with action today. That report review could be your edge. What are you waiting for in this market?