Homeowners across the United States are staring down a tough reality. Private insurers have pulled back sharply in areas hit hard by disasters, leaving many without standard policies. Four states top the list where reliable coverage has become elusive, pushing residents toward costly last-resort options.[1][2]

This shift stems from years of massive claims tied to extreme weather. Families now scramble for alternatives amid soaring costs. The problem shows no signs of easing as risks mount.[3]

Florida: Hurricane Hotspot in Freefall

Florida leads the pack with a staggering 280 percent jump in non-renewals from 2018 to 2023. Insurers fled after repeated hurricanes piled up losses, making private policies scarce for coastal homes.[1] Average premiums there could hit $8,458 by late 2026, nearly three times the national figure.[4]

Many turn to Citizens Property Insurance, the state-backed plan now dwarfing private markets. Home sales stall as buyers balk at the risks. Rebuilding after storms grows harder without solid backing.[2]

California: Wildfire Retreat Reshapes Markets

California’s inland counties saw the highest non-renewal rates in 2023, driven by wildfire threats. Major players like State Farm dropped thousands of policies after devastating blazes in 2017 and 2018.[1][3] Regulators eased rules to lure insurers back, yet premiums still climbed 16 percent since 2023, with another 16 percent eyed for 2026.

The FAIR Plan has ballooned as a fallback, but it offers skimpy protection at high prices. Homeowners harden properties with fire-resistant upgrades, yet coverage gaps persist. Southern California wildfires in early 2025 only deepened the pullout.[2]

Louisiana: Storms Pile On Endless Pressure

Louisiana recorded a 267 percent surge in non-renewals over five years through 2023. Nearly 20 insurers exited recently, battered by hurricanes like Ida.[1] Premiums average over $5,000 now, ranking third nationally for 2026 projections.

Claim denials hit 47 percent in 2024 alongside Florida and California. State plans strain under the load from constant Gulf threats. Residents face rebuilding hurdles that drag on for years.[2]

Flood exclusions leave even more exposed, as standard policies skip that peril. Coastal erosion adds to the woes.

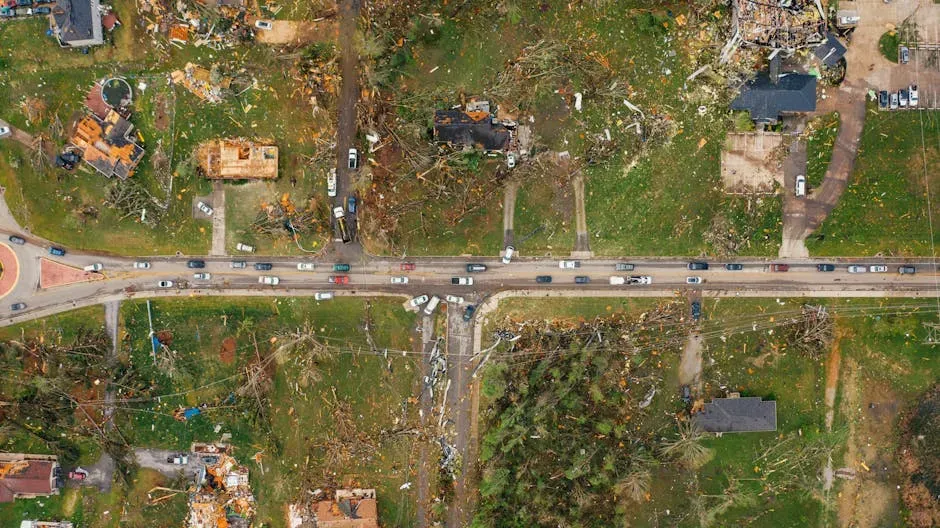

North Carolina: Coastal and Inland Alarms

Thirteen inland counties ranked among the top 100 nationwide for non-renewals in 2023. Hurricanes like Helene and Florence hammered areas far from the shore, spiking risks.[1][3] Nationwide dropped 10,000 coastal policies in 2024.

About a quarter of Helene claims closed without payout due to policy limits. Rates rose 14 percent since 2023, though regulators curbed bigger hikes. Homeowners inland now scramble as insurers eye broader retreats.[3]

Non-Renewals Explode Across the Board

Non-renewals climbed in 46 states during 2023 alone. Insurers shed over 1.9 million policies nationwide from 2018 to 2023.[2] High-risk zones bear the brunt, forcing shifts to pricier carriers.

This trend accelerated with record disasters that year. Lenders push forced-place insurance when gaps appear, hiking mortgage costs. Availability shrinks even in less obvious spots.[3]

Premiums Climb to Uncharted Heights

U.S. averages topped $2,900 in 2024, up 12 percent yearly. Florida homeowners brace for $8,400-plus bills by 2026 end.[4] Nebraska and Texas follow with four-figure jumps tied to hail and wind.

Midwest states like Illinois saw 48 percent rises since 2023. These burdens eat into budgets, some nearing 10 percent of income in worst spots. Affordability crumbles as losses mount.[3]

Climate Change Fuels the Fire

Warm oceans brew fiercer hurricanes, while dry conditions spark bigger wildfires. Insured losses averaged $100 billion yearly from 2023-2025, quadruple a decade prior.[3] Inland areas feel the spread, upending old assumptions.

Hail storms ravage Plains states more often. These shifts outpace pricing adjustments. Insurers now model future catastrophes, yet pullbacks continue.[2]

FAIR Plans Buckle Under Demand

These state insurers of last resort swell as private options vanish. California and Florida FAIR plans charge steep rates with thin coverage.[2] They lack full oversight, risking insolvency.

Homeowners pay more for less, facing high deductibles. Growth signals deeper market failure. Mitigation grants offer some relief, but not enough.[3]

Homeowners Bear Heavy Burdens

Uninsured rates doubled to 13.6 percent of homes by 2023. Denied claims leave repairs undone, homes unsafe.[2] Real estate freezes in hot zones.

Many retrofit for resilience, chasing discounts. Credit checks and loopholes complicate renewals. Daily life grinds amid uncertainty.[1]

Glimmers of Response Emerge

States tweak rules, like California’s catastrophe modeling. Building codes toughen in some spots. Twenty-six enacted insurance laws in 2025 sessions.[3]

Home hardening grants expand. Regulators eye rate transparency. Yet losses outstrip fixes for now. Progress hinges on bolder steps.[2]

The crisis underscores a simple truth. Homes remain vital, but protecting them demands adaptation from all sides. Quiet changes in how we build and insure may steady the ground ahead.