What is the Wealth Gap Rule?

Folks often talk about inflation eating away at money, but the Wealth Gap Rule takes it further by highlighting how everyday savings lose ground fast in 2026. It points to the simple math where inflation outpaces what banks pay on deposits, leaving regular people with less buying power by year’s end. Think about it this way: if prices climb around three percent over the year, your cash stash shrinks in real value even if it sits pretty in a savings account. Recent numbers show US consumer prices up three point three percent year over year as of March, and projections suggest it could nudge higher toward four percent by December. This rule isn’t some official policy; it’s the harsh reality playing out for millions who rely on savings for security. The gap widens because the wealthy park money in assets that beat inflation, while the rest watch their dollars dwindle. By December, that could mean your savings buy noticeably less at the store.

The term captures a broader trend where inequality grows as inflation hits the bottom harder. Global core inflation sits steady around two point eight percent, but in places like the US, it’s sticking higher with risks of upside surprises. Households feel it first in essentials, turning small savings into a losing bet over months. Central banks hiked rates before, but now with sticky prices, relief feels distant. This rule warns that without action, a year’s worth of erosion compounds quickly. People saving for emergencies or big purchases face the brunt, as cash loses about one percent every few months against rising costs. It’s a wake-up call baked into 2026’s economic mix.

Inflation Trends Heating Up

Inflation didn’t vanish after the big peaks; it’s lingering around levels that chip away at stability. In the US, the consumer price index rose three point three percent in the twelve months to March 2026, up from February’s two point four percent. Projections from groups like J.P. Morgan peg global core at two point eight percent for the year, but some forecasts warn of four percent or more by December. Food prices ticked up zero point one percent from February to March alone, sitting two point seven percent higher year over year. This steady climb means every trip to the grocery store costs more, squeezing budgets tight. Emerging markets face even steeper hits from currency drops, making imports pricier across the board. By mid-year, many feel the pinch building toward that potential twenty percent real loss if trends accelerate.

Higher energy and supply issues keep pushing forecasts upward, with G20 inflation now at four percent expected. The Federal Reserve’s latest projections show bands up to three point seven percent, signaling uncertainty. Households adjust by cutting back, but the damage to savings accumulates quietly. Past years saw global peaks over eight percent, and while lower now, the momentum persists. Central banks hold rates steady to tame it, but upside risks loom large. This environment turns time into an enemy for anyone holding cash. December could bring a stark reminder of how far twenty percent inflation erosion feels in daily life.

How Savings Accounts Are Losing

High-yield savings accounts offer up to five percent APY in May 2026, but most folks don’t chase those top rates. Average accounts pay far less, often below three percent, leaving them underwater against inflation. At three point three percent CPI, your money loses purchasing power monthly if interest lags. Over seven months to December, that gap could eat several percent in real terms, heading toward the headline’s warning. Banks like Vio or LendingClub hit four percent, yet billions sit in low-yield spots from big institutions. Inflation at five percent annually halves value over a decade, but short-term hits feel immediate too. People check balances and see numbers grow nominally, missing the silent shrink in what it buys.

Cash savings erode fastest during these periods, as provided facts note significant drops within a year. Even with rates elevated from past hikes, they trail projections for year-end inflation. Retirees and conservative savers suffer most, watching nest eggs deflate. Online banks push competitive yields, but switching takes effort many skip. The Wealth Gap Rule shines here: assets like stocks often outrun inflation, but plain savings don’t. Projections show core PCE around three percent, still outpacing typical returns for many. By December, that twenty percent feel becomes real for unprotected funds.

Food and Essentials Surge

Grocery bills keep climbing, with food prices up two point seven percent year over year in March 2026. Cumulative rises topped twenty percent from 2021 to 2024 in many spots, and 2026 adds more pressure. USDA sees all food up two point nine percent last year, with at-home groceries slower but still rising. Eggs and staples fluctuate, but overall trends point higher into year-end. Families stretch dollars thinner, dipping into savings for basics. Pet food up eight point two percent, baby food seven point five, show no mercy across categories. This fuels the rule’s impact, as daily needs drain cash faster.

Predictions for 2026 grocery hikes around three point one percent mean holidays cost more come December. Inflation in beverages and cereals adds up, turning carts into budget battles. Global food pressures from weather and trade keep supplies tight. Households cut portions or switch brands, but prices win out. Savings meant for extras now cover meals, accelerating the wealth erosion. Emerging economies see even wilder swings from imports. The twenty percent drop hits home hardest through these rising shelves.

Wages Lagging the Curve

Real average hourly earnings rose just zero point three percent from March 2025 to 2026, barely keeping pace. Nominal wage growth hovers around three point five percent, but inflation nibbles it away. Low-wage workers saw three point five percent rises, yet core inflation edges higher. Many regions show wages trailing, reducing real take-home power. This disconnect means even raises feel flat at checkout. Productivity-pay gaps widen, echoing long-term trends. Savings buffers shrink as income barely covers costs.

Forecasts suggest salary budgets might outpace inflation slightly, but recent CPI spikes threaten that. March data shows weekly wages up three point five percent against three point three inflation, a slim margin. Lower quartiles struggle most, widening the gap. Job switchers gain more, but stickiness keeps averages down. Global real wages lagged post-2022 hikes, continuing into now. By December, stagnant real income amplifies savings loss. The rule thrives on this mismatch between pay and prices.

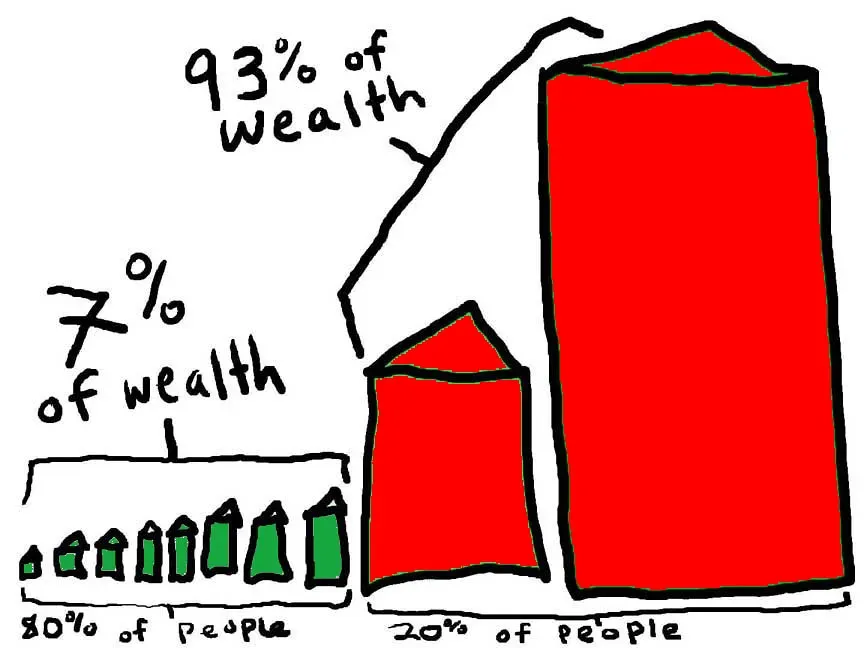

Wealth Inequality Widens

The top one percent holds nearly one-third of US wealth as of late 2025, a record high. Billionaires’ net worth tops two point seven trillion for the top twelve alone. Poorest in top one percent gain vastly more than bottom quintile richest. Global top zero point zero zero one percent owns outsized shares, per inequality reports. Assets like housing and stocks surge past wages, favoring the rich. This dynamic supercharges the Wealth Gap Rule for average savers. Inequality reports for 2026 confirm persistence at extreme levels.

Racial and generational gaps grow under current policies, with top earners pulling ahead. Younger families see percentage gains from low bases, not true catch-up. Multimillionaires triple average holdings, leaving cash-holders behind. Housing prices outpace incomes, locking many out. The rich diversify into inflation-beaters, while others hold depreciating cash. By December, this divide makes twenty percent losses feel personal. Trends show no quick reversal in sight.

Borrowing Costs Bite Harder

Higher rates from 2022-2024 lingers, with mortgages at decade highs. Borrowing for homes or cars now demands more interest, diverting savings. Central banks like the Fed hold steady amid sticky inflation. This raises monthly payments, forcing dips into emergency funds. Consumer spending slows as costs mount. The rule amplifies as debt service eats real income. Projections keep rates elevated through year-end.

Credit card and loan rates follow suit, punishing overextended households. Adjustable debts reset higher, straining budgets further. Savings go toward interest, not growth. Wealthy refinance or invest differently, escaping the trap. Average borrowers face compounded pressure into December. Global patterns mirror this, with emerging markets hit worst. The twenty percent erosion includes these hidden drains.

Steps to Bridge the Gap

Shift some savings to high-yield accounts topping four to five percent APY. Shop online banks for better rates without fees. Consider inflation-protected bonds or diversified investments. Track spending to cut waste, padding real power. Build side income streams that outpace costs. Review budgets monthly against CPI updates. These moves counter the rule’s toll before December hits.

Assets like stocks historically beat inflation long-term, though volatile. Gold or commodities hedge rises too. Automate transfers to growth spots now. Educate on compound effects early. Communities share tips for collective resilience. Stay informed on Fed moves for timing. Small shifts compound to protect against that twenty percent sting.